Crop "Insurance" is a Misnomer

It’s a complete misnomer even to call the federal crop insurance program “insurance.” It works nothing like the private insurance market because taxpayers pay about 60 percent of the premiums, all the costs of administering the program and a large share of the claims payouts. Moreover, what crop insurance deems a “loss” bears little resemblance to any actual financial losses a farm family experiences. The cost to growers is so low that over time most can expect to collect far more in payouts than they pay in premiums. In other words, most farmers make money by just by buying a crop insurance policy.Farmers Make Money On It

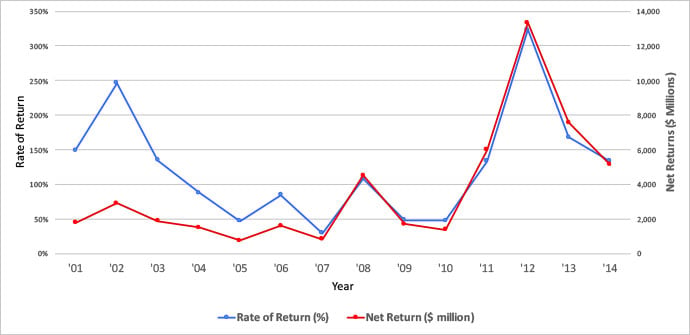

Between 2000 and 2014 farmers, in aggregate got back $2.20 in claims for each dollar they paid in premiums, an annual return of 120 percent. In aggregate, farmers enjoyed positive rates of return every year, ranging from 29 percent ($1.29 for every dollar of premium in 2007) to 324 percent ($4.24 for every dollar of premium in the 2012 drought year.)

A Gamble That's a Good Bet

Making more in payouts than growers pay in premiums is not a sure thing. Not all farmers enjoy a positive rate of return every year, and the rate of return varies dramatically across crops and regions. But the odds are in the growers’ favor, because premiums are so over-subsidized. It amounts to placing a bet in a casino where the size of the house’s money doubles your bet.Back to Basics

Federal crop insurance can and should be a fiscally and environmentally responsible safety net that steps in when farmers suffer real financial losses that threaten the viability of their business. But that’s not what the program is today. Congress needs to step up and reform the program so that it works for taxpayers and the environment as well as it does for farmers.

Source - ewg.org